The history of American business is littered with companies whose reputations fell apart overnight. But it's rare for a company with a history as long and august as Wells Fargo's to suffer so quick and thorough a fall. It's a Main Street bank, meaning that by and large it makes its money by selling services to individuals and small businesses—checking accounts, savings accounts, mortgages, safety deposit boxes. From its beginnings as a cross-country express service in 1852, the company evolved into a regional powerhouse, and from there, to one of the biggest retail banks in the world.

But today, for many people, the name Wells Fargo stands for scandal. A key part of Wells Fargo's business strategy is cross-selling, the practice of encouraging existing customers to buy additional banking services. Customers inquiring about their checking account balance may be pitched mortgage deals and mortgage holders may be pitched credit card offers in an attempt to increase the customer's profitability to the bank.

Other banks have attempted to emulate Wells Fargo's cross-selling practices . The bank would be difficult for someone in the service industry or other jobs that require depositing cash frequently. Users who do need to deposit cash can do so by taking it to a bank and getting a money order, which can be deposited by Photo Check Deposit. Simple does not offer personal checks — not an issue for me as I pay my rent online and haven't written a check in several years.

In January 2020, Treasury Department officials issued a report on the Wells Fargo account scandal. John Stumpf got a $17.5 million fine and a lifetime ban from the banking industry. This all came two years after the Fed had kept the bank's assets, just under $2 trillion, as punishment.

In September 2016, Wells Fargo was issued a combined total of $185 million in fines for opening over 1.5 million checking and savings accounts and 500,000 credit cards on behalf of customers without their consent. The Consumer Financial Protection Bureau issued $100 million in fines, the largest in the agency's five-year history, along with $50 million in fines from the City and County of Los Angeles, and $35 million in fines from the Office of Comptroller of the Currency. The scandal was caused by an incentive-compensation program for employees to create new accounts. It led to the firing of nearly 5,300 employees and $5 million being set aside for customer refunds on fees for accounts the customers never wanted.

Carrie Tolstedt, who headed the department, retired in July 2016 and received $124.6 million in stock, options, and restricted Wells Fargo shares as a retirement package. Wells Fargo will bring together multiple national and community stakeholders to roll out the broad-based initiative that is designed to increase access to affordable products, digital banking and financial guidance within unbanked communities. Through this initiative, Wells Fargo also will collaborate with partners to explore solutions to the credit challenges facing unbanked individuals. This year, the bank will work with partners to set and begin measuring a 10-year goal for reducing the number of people who are unbanked, with milestones along the way.

But when the news broke that the company had been creating unauthorized accounts to collect fees and pushing employees to offer unnecessary services to customers, I felt a bit queasy about my bank. Wells's stock price soared, and Tolstedt, whose salary was $1.75 million, received more than $20 million in annual bonuses from 2010 to 2015, which was justified in part by the "record cross-sell results" in her division, said Wells in its financial filings. But Stumpf and the rest of the executive team, and soon the board, knew there were issues. In 2011, a group of bankers who were terminated for sales violations wrote a letter to Stumpf, arguing that their actions had not only been condoned by management in their branch, but that similar things were happening across the bank.

Lisa Stevens, who became the head of the West Coast region in 2010 and reported directly to Tolstedt, was complaining by 2012 to the bank's corporate chief risk officer, Mike Loughlin, about "unrealistic sales goals and her frustration with Community Bank leadership," according to the board report. There were "morning huddle" meetings to discuss "Daily Solutions," or sales goals for the day, and a manager would do hourly check-ins to see if each banker was making progress toward his or her quota, which in 2008 was eight products per day. (The number was increased in 2010 to 8.5.) "Call nights" were scheduled after the branch closed to "help" bankers who were having trouble meeting their sales goals, which were challenging in St. Helena. According to an analysis that was done for a lawsuit Guitron later filed, there were only about 11,500 potential customers in the area, and 11 other financial institutions.

The quotas for the bankers at Guitron's branch totaled 12,000 Daily Solutions each year, including almost 3,000 new checking accounts. Initially, the company tried to play it off as the work of a few bad apples. Further investigations revealed that Wells Fargo branch employees were under incredible pressure to sell more products to more customers.

Senior executives threatened branch managers, branch managers threatened their staff—they were pushed to go for great, as if their jobs were on the line every day. They came from the communities they served, and they needed the jobs they had, so they tried their best to meet those unrealistic quotas. It was underpinned by the financial reality that customers who had, say, lines of credit and savings accounts with the bank were far more profitable than those who just had checking accounts. In 1997, prior to Norwest's merger with Wells Fargo, Kovacevich launched an initiative called "Going for Gr-Eight," which meant getting the customer to buy eight products from the bank. Community banking net income was $7.4 billion in 2019 on total annual revenue of $85 billion.

Wells Fargo, the San Francisco-headquartered banking titan, has come under fire from seemingly all angles after creating nearly 2 million fraudulent bank and credit card accounts for customers without their permission. In the wake of its fraud, Wells Fargo has been through the ringer. The Bank has settled civil charges with the city and county of Los Angeles, been charged with $185 million in fines, refunded close to $2.5 million to customers for the wrongful fees it charged, and received subpoenas from three different United States Attorneys' offices. Wells Fargo was regarded for years as one of America's best banks. The bank admitted that employees had opened as many as 3.5 million phantom accounts in customers' names to meet stratospheric sales goals.

It also admitted forcing customers to buy unneeded auto insurance and charging improper mortgage fees. I overdrafted my Wells Fargo account multiple times after forgetting to transfer a couple of stray recurring bills to my new debit card. I attempted to set up direct deposit for my paycheck last month, but per company policy I received a physical check in the mail to verify the account switch. When I deposited the check through the Simple app on my phone, Simple said it would take nine business days to clear, making it impossible to pay my rent on the first of the month. This part of the bank's operations services retail and small business clients with their everyday banking needs. Some of the services include checking and savings accounts, loans, mortgages.

The bank serves these clients in its branches and by way of its automated teller machines . Wells Fargo coined the phrase, "Go for Gr-Eight" – or, in other words, aim to sell at least 8 products to every customer. The board chose to use a clawback clause in the retirement contracts of Stumpf and Tolstedt to recover $75 million worth of cash and stock from the former executives.

Wells Fargo has gravely wronged its customers and stakeholders, but it has not yet done enough to make up for its blatant breach of trust. Surely the fine Wells Fargo will pay and the return of wrongly-charged fees is a financial hit to the Bank, but these punishments do not address the fundamental issues that led to the fraud in the first place. Taking a "bottom-up" approach by firing employees at the retail banking level does not solve the problem of pressure from above to cut corners. Rather, Wells Fargo needs to consider changing itself, its culture, its compensation practices, its commitment to ethical banking, from the top down.

Top down change starts with an assumption of responsibility by the Bank's senior leadership. Only when those with the power to effectuate change at Wells Fargo take responsibility to do so will constructive change happen. Wells Fargo markets itself as the "Main Street" bank, offering a broad range of financial and banking solutions to its nearly 40 million customers; indeed, one of the Bank's main value propositions has been cross-selling customers on the many services it provides. In wake of the sham account scandal, though, that reputation has taken a hit. Customers are reeling from being charged improper fees on accounts opened without their permission, and in some cases, having their credit scores negatively impacted.

With more than 25 percent of its branches in LMI community census tracts, Wells Fargo will introduce a new program within LMI neighborhood branches that will be designed around the needs of the diverse communities it serves. The branches will feature redesigned spaces created to deliver one-on-one consultations, improve digital access and offer financial health seminars, and through these efforts, will help build trust. Wells Fargo will select a set of pilot locations to introduce the program, with a plan to expand to 100 LMI neighborhood branches with a high concentration of unbanked individuals. Wells Fargo will work closely with Fintechs that are deeply committed to helping underserved communities. For instance, Wells Fargo is among the investors in Greenwood, a digital platform for Black and Latino individuals and business owners.

The bank also has started a collaboration to help the Fintech MoCaFi provide banking to unbanked individuals, starting with offering MoCaFi customers the ability to use their MoCaFi debit card at Wells Fargo ATMs without incurring fees from Wells Fargo. Wells Fargo will increase awareness and outreach about low-cost, no overdraft fee accounts, such as Wells Fargo's Bank On-certified Clear Access Banking. Wells Fargo introduced Clear Access Banking in 2020, offering an affordable account designed for those who are new to banking or have encountered past challenges opening or keeping a bank account. Florida Gulf Coast University and Wells Fargo have teamed up to offer you optional banking convenience with your linked FGCU Debit Card. Use it for your day-to-day financial needs on and off campus when it's linked to a Wells Fargo checking account, with two account options ideal for students.

Enjoy no-fee access to Wells Fargo ATMs nationwide, including the Wells Fargo ATMs on campus. Make everyday purchases and pay bills at participating retailers and service providers. Wells Fargo promised to refund customers who had improper fees as a result of this business practice and fired 5,300 employees. According to the New York Times, Wells Fargo paid "more than $1.5 billion in penalties to federal and state authorities and $620 million to resolve lawsuits from customers and shareholders." When a multinational with tens of millions of dollars in cash on its balance sheet needs somewhere to store that cash, Wells Fargo's wholesale division is where they do business.

To be a Wells Fargo wholesale customer, you need annual revenues of at least $5 million. Wells Fargo's wholesale operations have even greater reach than its community operations do. The bank has wholesale offices in 42 states that are manned by more than 30,000 employees. That's to say nothing of its wholesale offices across the globe, from Santiago to Seoul, Calgary to Cairo, and Sydney to St. Helier. All told, net income from wholesale banking totaled $10.7 billion in 2019—far more than wealth, brokerage, and retirement operations.

The firm's primary subsidiary is Wells Fargo Bank, N.A., a national bank chartered in Wilmington, Delaware which designates its main office in Sioux Falls, South Dakota. It is the fourth largest bank in the United States by total assets and is one of the largest as ranked by bank deposits and market capitalization. Along with JPMorgan Chase, Bank of America, and Citigroup, Wells Fargo is one of the "Big Four Banks" of the United States. The initiative will focus on reaching unbanked communities and, in particular, helping remove barriers to financial inclusion for Black and African American, Hispanic, and Native American/Alaska Native families, which account for more than half of America's 7 million unbanked households1.

It also will assist those who are underbanked or underserved – individuals who may have a bank account yet continue to use high cost, non-bank services and have similar needs. In February 2020, Wells Fargo agreed to pay $3 billion to settle criminal and civil investigations into a long-running practice whereby company employees opened millions of unauthorized bank accounts in order to meet unrealistic sales goals. A personal banker who works in a North Carolina branch said his manager had told him to increase his referrals to the bank's mortgage team and financial advisers. He said he had ethical qualms about trying to sell more products to his customers, who are mostly college students and retirees with limited money. Paradoxically the hard-core sales culture seemed to intensify once Stumpf took over.

In 2010, both the compensation and performance ratings systems were rejiggered so that they were associated with sales goals. Bankers, branch managers, and district managers risked pay cuts and poor performance reviews if they didn't hit the goals, noted the board report, and employees were ranked against one another. Wells Fargo swallowed up Wachovia during the financial crisis, to become the country's third-largest bank by assets, and its soaring stock made it worth almost $300 billion. John Stumpf, a native Minnesotan who could have played a modern George Bailey, took over as C.E.O. when Kovacevich retired, at the end of 2007.

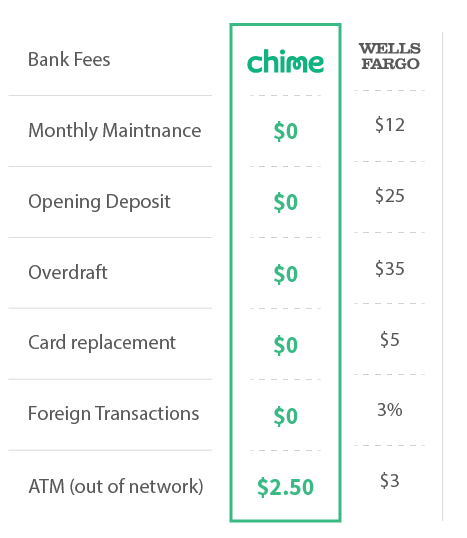

He, like Kovacevich, repeatedly cited Wells Fargo's success at cross-selling as a reason investors should value the bank's stock—and they believed. "In the eyes of Wall Street, Wells has always been a cut above," says one longtime bank investor. Unlike the other big banks, it positioned itself as "the bank of the real economy," i.e., its major business was retail banking for everyday folks, not trading or investment banking for sophisticated investors. It helped that Warren Buffett's Berkshire Hathaway has long been the bank's biggest shareholder. Our overdraft fee for Consumer checking accounts is $35 per item ; our fee for returning items for non-sufficient funds is $35 per item. We charge no more than three overdraft and/or non-sufficient funds fees per business day.

Overdraft and/or non-sufficient funds fees are not applicable to Clear Access Banking℠ accounts. The payment of transactions into overdraft is discretionary and we reserve the right not to pay. For example, we typically do not pay overdrafts if your account is overdrawn or you have had excessive overdrafts. 7,757 Financial Advisors work in the traditional brokerage channel of Wells Fargo Advisors through Wells Fargo Clearing Services, LLC, with branch offices located in all 50 states and the District of Columbia. In addition, the firm's in-bank brokerage channel includes 3,227 Financial Advisors and 4,884 Licensed Bankers located in Wells Fargo bank branches. The clearing operations of Wells Fargo Clearing Services, LLC provide operational, clearing, and related consulting services for the affiliated Wells Fargo retail brokerage business and approximately 53 unaffiliated brokerage firms.

Retail banking consists of basic financial services, such as checking and savings accounts, sold to the general public via local branches. Times reported that desperate branch employees opened fake accounts and credit cards in order to meet their sales quotas. It was only three years later in 2016 that the company admitted that over 3.5 million unwanted accounts were opened. This segment services business clients and high-net-worth individuals by offering them wealth management services, as well as investment and retirement products. Some of these services include financial planning, credit, and private banking.

Wells Fargo's current and former employees claim an inconsistent company culture was the driving force behind the creation of the nearly 2 million sham accounts that resulted in nearly 5,300 employees' terminations of employment. Further, branch managers who hit their sales targets were rewarded handsomely, sometimes with bonuses of up to $10,000. The tech company has abandoned plans to offer checking accounts in partnership with banks and will instead focus on being a technology provider for them.

Citigroup says it will press ahead with aspects of the digital banking project on its own. Wells Fargo will broaden its collaboration with CFE Fund and local Bank On coalitions to pilot new strategies and approaches that help overcome barriers to banking access in several markets with high concentrations of unbanked households. The program will focus on helping those who are unbanked navigate the financial system, develop an easier, more seamless path for them to open a Bank On-certified account and access services they need within mainstream banking.

It will be used to identify best practices that can be applied on a national scale. Wells Fargo will deepen its existing relationships with Black-owned Minority Depository Institutions to support their work in the communities they serve, including outreach efforts and providing the option for their customers to withdraw cash from Wells Fargo's ATMs and incur no Wells Fargo fees. In addition, Wells Fargo is offering access to a dedicated relationship team that will work with each MDI on financial, technological and product development strategies to help strengthen and grow their institutions.

About 100,000 positions could vanish over the next five years as large U.S. banks invest more in digital banking and other technologies, Wells Fargo analysts predicted in a research note this week. Roles slated to disappear include branch managers, call center employees and tellers. Artificial intelligence, cloud computing and robots will play a larger role in daily banking functions like taking payments, approving loans and detecting fraud. Gory South Korean drama "Squid Game" is its number one show in the U.S., and huge around the world. Capital One Financial Corp., which closed 68 branches in October including 26 in New York and 15 in Texas, has been rationalizing its branches for some time. Capital One significantly expanded its online deposit-gathering capability with the 2012 purchase of ING Bank FSB, and the company has continued to pursue digital offerings that can help it compete against branch-based retail banks, according to Chairman, CEO and President Richard Fairbank.

Wells Fargo's own analysis found that between 2011 and 2015 its employees had opened more than 1.5 million deposit accounts and more than 565,000 credit-card accounts that may not have been authorized. Some customers were charged fees on accounts they didn't know they had, and some customers had collection agencies calling them due to unpaid fees on accounts they didn't know existed. Gaming was so widespread that it had even spawned related terms, such as "pinning," which meant assigning customers personal-identification numbers, or PINs, without their knowledge in order to impersonate them on Wells Fargo computers and enroll them in various products without their knowledge.